The latest issue of Finance Dublin contains a series of articles by the heads of the biggest representative bodies in the financial services industry and leading company directors' institutes about the most radical set of proposals for reform of the regulation of the industry since the Great Financial Crisis - the Individual Accountability Framework (IAF). They paint a clear picture of growing unease about the framework with the bodies calling for more time to assess the IAF's potential consequences, for examination of possibilities for reform, and for a postponement of the measures until mid 2024 at least.

Regulation was cited as one of the key reasons behind the erosion of Ireland's attractiveness as a hub for international insurance in an Insurance Ireland-commissioned report by Milliman, presented at the European Insurance Forum. The broader cost of doing business and talent shortages were also identified to help invigorate Ireland's cross-border insurance industry.

The dangers in the delay of revamping aspects of Ireland's corporate tax regime feature with The Irish Tax Institute President Tom Reynolds expressing disappointment (he is joined in this by BDO's Angela Fleming in the Irish Tax Monitor) that the introduction of territorial tax elements to the Irish regime has been decoupled from the introduction of BEPS rules.

While the introduction of BEPS around the world continues, with the Irish Government's BEPS Pillar II legislation contained in the Finance Bill, in this month's issue we feature the potential channels for resolving tax disputes under the new international tax rules. How to best use the time afforded by the likely delay to the introduction of the EU's ViDA reforms also feature as do the main Budget points for the financial services industry including interest deductiblity rules, the bank levy and newly enhanced R&D regime.

The Finance Dublin Annual Accountancy Survey shows a year of strong fee income growth amongst Ireland's leading firms and big changes at the top of the table. The figures for latest year ends ending in 2022 and 2023, show Republic of Ireland fee income growth of 17% for 2022-3 with a new leader as all of the Big Four firms switch places in terms of their size and growth rankings at the top.

The "Agile" software project management system can also be applied to complex financial services projects. EY's Jeff Cowhig and Kieran Hanley assess the possibilities, with examples of its successful application in FS.

The 2023 edition of the Finance Dublin Yearbook, the annual print & E paper snapshot of Ireland's financial services centre - including the world's 3rd largest funds centre, the 6th largest financial services exporter, and with our updates of the significant developments in the profiles of the top 500+ financial services companies and institutions in Ireland.

The Yearbook's 2023 Review & Outlook provides an overview of the 'state of the centre' - reflecting a year of exceptional progress as IFS industry in the jurisdiction of Ireland deepened and strengthened, despite the headwinds caused by monetary tightening in global financial markets. This is covered in a series of analytical articles in the publication, featured here.

The Yearbook contains the 2023 Finance Dublin Yearbook's Professional Services Guide, with its Who's Who of advisers and practitioners in the jurisdiction.

The full E-Paper edition can be accessed by subscribers HERE.

With uncertainty around the makeup and timeline of the EU's Unshell Directive Maple's Lynn Cramer assesses the current proposals and demands on in-scope entities. With the proposed implementation date of 1 January 2024 now likely slipping to 2026, she says, 'Given the general desire of taxpayers for stability (and, yes, certainty), the two year back and forth in relation to these proposals is highly unsatisfactory. That is particularly true given that aspects of the proposals involve a review of activities and fact patterns during a lookback period (of one year, or two - yet more uncertainty).'

Despite uncertainty around timelines for the EU's ATAD 3 (the Unshell Directive) Deloitte's Anna Holohan outlines the actions that can be taken now in preparation for the new rules so that entities can demonstrate substance or ease compliance with the proposed reporting standards that could be required.

BDO's Mark O'Sullivan outlines the changes and implications for companies availing of the R&D Tax Credit following significant updates by the Revenue Commissioners, and the considerations companies availing of the credit need to take when deciding to opt-in to the new rules during the transition period.

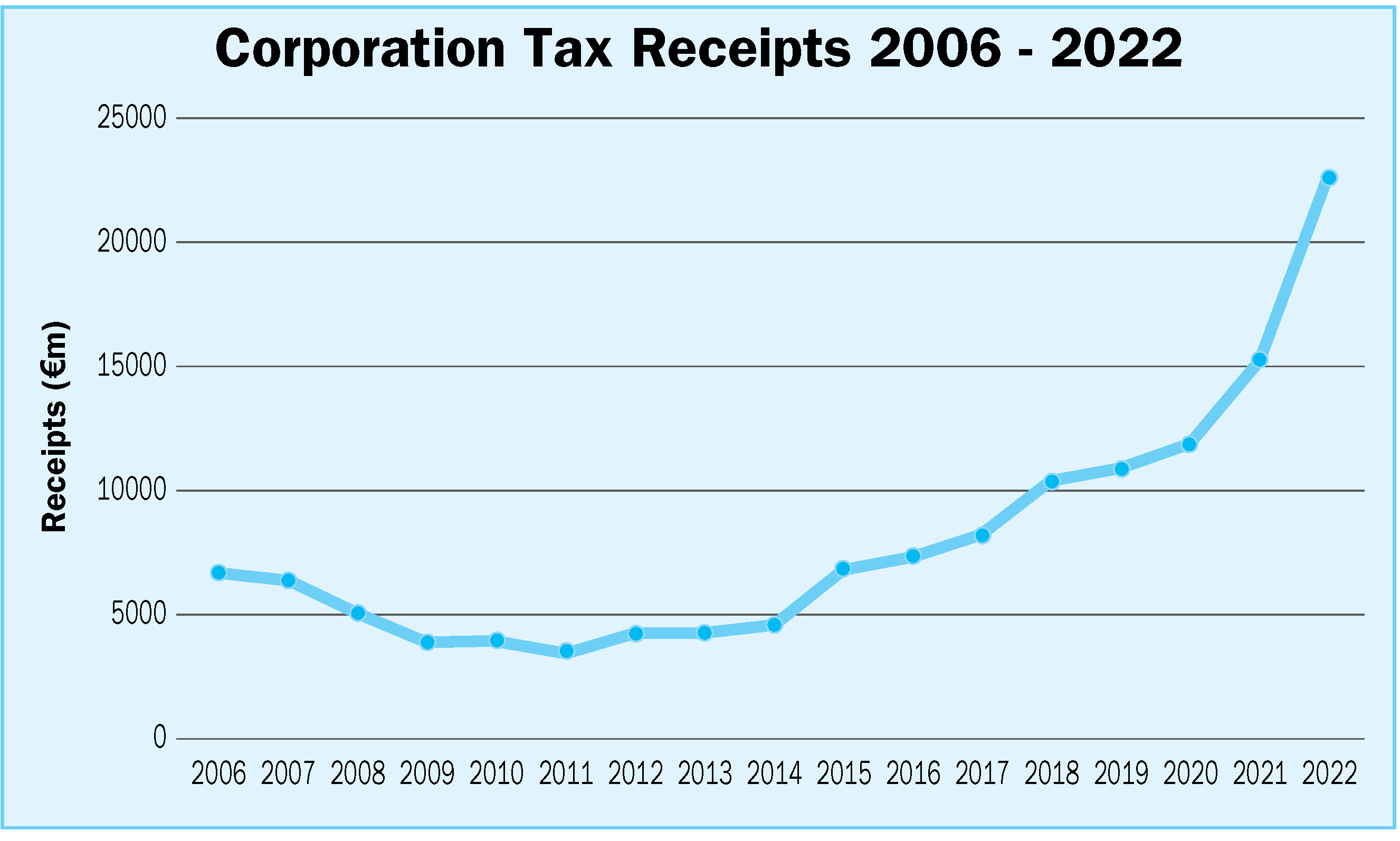

July saw the publication by the Department of Finance of data on the background to the 2024 Budget, in the Tax Strategy Group papers. This article puts forward a hypothesis positing why, after 2016, there has been an acceleration of the growth in the Corporation Tax yield.

As a result of the latest BEPS guidance from the OECD new areas of concern are beginning to come into focus for stakeholders, with one such areas, aircraft lessor's ability to avail of BEPS SBIE examined in detail in this month's Irish Tax Monitor. Life insurance, and in particular the treatment of the Ireland-specific 'old basis business', is also raised as an area that requires guidance in relation to BEPS rules. Other topics featuring this month include ESG and the tax function; the EU's Carbon Adjustment Mechanism, simplifying Ireland's interest deductibility rules, VAT developments and the latest key TAC decisions.

The prospect of Double Taxation of US corporates in Ireland has been raised by the American Chamber of Commerce in Ireland if the proposed QDTT to level up Irish corporation tax to 15% for qualifying (large) companies is not recognised as creditable foreign tax in the US.

Writing in the latest issue of the Irish Tax Monitor, Louise Kelly, Partner, Corporate and International, Corporate Tax, Deloitte Ireland LLP (pictured) says: "both sides of the political divide in the US may coalesce around the need to give an FTC for the QDTT to ensure that US groups are not financially disadvantaged; it is perhaps the one aspect of Pillar Two on which it could be hoped that a consensus would be reached at an early stage".