YEARBOOK & DIRECTORY

Finance Dublin Yearbook 2023

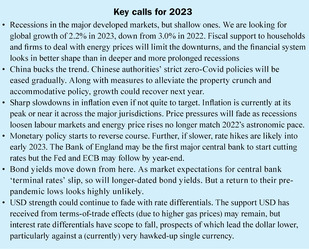

2023 outlook: shallow recessions, lowering inflation and late year interest rate cuts

Investec’s Aisling Dodgson says policy responses to dampen rising prices mean we are likely at, or nearing, peak inflation. While the headwinds of labour shortages, supply chain constraints and geopolitics knock global GDP estimates, there is optimism that the latter half of 2023 could see Central Banks beginning to bring interest rates down.

After three decades of largely subdued global price pressures, 2022 was a year when inflation returned with a vengeance. Central banks eventually responded by raising policy rates more aggressively. Global bond markets have been volatile, not least given huge repricing at the shorter end of the curves. Given the considerable degree of monetary tightening that has now taken place and an ensuing period of softer global growth, we are likely to be at or very close to peak inflation in developed markets (DMs).

Labour shortages are also aggravating the situation in DMs, fuelled in many cases by falling participation rates. The precise reasons for shrinking labour forces are not 100% clear but some factors seem to include; ill health (as hospitals cope with Covid backlogs); a switch in work/life balance preferences; early retirement (especially when asset markets were more buoyant and boosting pension values); and a rise in students. A key judgement is that we expect participation to recover. Many health issues (we hope) should be resolved in time and a harsher economic climate may encourage many to return to work.

Supply chain issues have also dogged the world economy, not least due to China’s zero Covid policy. An uber stringent Beijing has in recent weeks started to loosen their draconian Covid restrictions and as a result activity looks to be picking up now in some key cities but the urban-rural migration that is traditional over Lunar New Year could spark a new wave of difficulty in other parts of the country.

Global supply chain strains seem to have eased in recent months too and China’s lockdown stance will be a determining factor on whether this direction is maintained over 2023. Our guess is that a vaccination drive will reinforce what already seems like a successful (so far) relaxation of its Covid laws.

Another ongoing geopolitical issue is the war in Ukraine. The Ukrainians have regained ground in the east and south of the country, while the threat of Russian deployment of nuclear weapons has dissipated. There is however still a big question mark over Putin’s endgame and so the conflict will likely continue to cloud the outlook in 2023.

We see few reasons to alter our existing view of 2023 prospects. The various headwinds, especially tighter monetary conditions, pull global GDP growth down to 2.2% from 3.0%, with much of the DM space in recession. An exception to the trend is China, where growth steps up to 4.4% from 3.0%, helped by a new booster vaccination drive, greater tolerance of Covid cases and fewer lockdowns. This also helps to reduce logjams in global supply chains, albeit gradually. Also, labour market strains ease, partly due to layoffs but also as participation improves. This helps inflation to retreat from double digit levels in many jurisdictions.

Our assessment is that spare capacity will build sufficiently for central banks to be back on track to meet their inflation targets. In some areas e.g., US & UK central banks should be able to begin to bring rates down by end-2023. Indeed, we continue to view yield curves to be too steep. One question is whether major central banks persist in reducing their balance sheets through 2023, perhaps even after beginning to cut policy rates. We note that unlike 2008 / 2009, banks are functioning properly, so that as central banks cut rates when inflation pressures are sufficiently under control, demand will recover.

We do stress that adequate labour market and supply chain capacity are critical, so that higher demand turns into growth and not inflation. If not, central banks’ ability to stimulate the world economy could remain limited.

Aisling Dodgson

Labour shortages are also aggravating the situation in DMs, fuelled in many cases by falling participation rates. The precise reasons for shrinking labour forces are not 100% clear but some factors seem to include; ill health (as hospitals cope with Covid backlogs); a switch in work/life balance preferences; early retirement (especially when asset markets were more buoyant and boosting pension values); and a rise in students. A key judgement is that we expect participation to recover. Many health issues (we hope) should be resolved in time and a harsher economic climate may encourage many to return to work.

Supply chain issues have also dogged the world economy, not least due to China’s zero Covid policy. An uber stringent Beijing has in recent weeks started to loosen their draconian Covid restrictions and as a result activity looks to be picking up now in some key cities but the urban-rural migration that is traditional over Lunar New Year could spark a new wave of difficulty in other parts of the country.

Global supply chain strains seem to have eased in recent months too and China’s lockdown stance will be a determining factor on whether this direction is maintained over 2023. Our guess is that a vaccination drive will reinforce what already seems like a successful (so far) relaxation of its Covid laws.

Another ongoing geopolitical issue is the war in Ukraine. The Ukrainians have regained ground in the east and south of the country, while the threat of Russian deployment of nuclear weapons has dissipated. There is however still a big question mark over Putin’s endgame and so the conflict will likely continue to cloud the outlook in 2023.

We see few reasons to alter our existing view of 2023 prospects. The various headwinds, especially tighter monetary conditions, pull global GDP growth down to 2.2% from 3.0%, with much of the DM space in recession. An exception to the trend is China, where growth steps up to 4.4% from 3.0%, helped by a new booster vaccination drive, greater tolerance of Covid cases and fewer lockdowns. This also helps to reduce logjams in global supply chains, albeit gradually. Also, labour market strains ease, partly due to layoffs but also as participation improves. This helps inflation to retreat from double digit levels in many jurisdictions.

Our assessment is that spare capacity will build sufficiently for central banks to be back on track to meet their inflation targets. In some areas e.g., US & UK central banks should be able to begin to bring rates down by end-2023. Indeed, we continue to view yield curves to be too steep. One question is whether major central banks persist in reducing their balance sheets through 2023, perhaps even after beginning to cut policy rates. We note that unlike 2008 / 2009, banks are functioning properly, so that as central banks cut rates when inflation pressures are sufficiently under control, demand will recover.

We do stress that adequate labour market and supply chain capacity are critical, so that higher demand turns into growth and not inflation. If not, central banks’ ability to stimulate the world economy could remain limited.

Aisling Dodgson is Head of Treasury Products & Distribution at Investec Europe.