YEARBOOK & DIRECTORY

Finance Dublin Yearbook 2023

REVIEW & OUTLOOK 2022-2023

It may not seem like boom times, but the outlook remains positive for Ireland’s financial services industry

As 2023 dawns, the FS industry is operating in a world that still is dominated by a major European war, with consequent reverberations in markets, notably in the form of the twin threats of recession and inflation. These are set to continue to remain themes in the markets that Ireland’s open economy exists and thrives in, in 2023 but underlying this, the pulse of business remains strong in Ireland’s financial and professional services industries.

For the financial services industry the repressed post Covid global economic outlook also continues to overhang markets, and this is reflected in consolidation moves affecting the Irish-domiciled industry, as well as uninterrupted technical change developments in fintech, in asset management, insurance, capital markets and finance.

Supplementing these trends is a regulatory and governance agenda that can provide a basis for all those working in the industry and in the 500 plus enterprises and bodies profiled in this Yearbook, with a regulatory framework that can offer huge business opportunities for a globally focused industry.

For the financial services industry the repressed post Covid global economic outlook also continues to overhang markets, and this is reflected in consolidation moves affecting the Irish-domiciled industry, as well as uninterrupted technical change developments in fintech, in asset management, insurance, capital markets and finance.

Supplementing these trends is a regulatory and governance agenda that can provide a basis for all those working in the industry and in the 500 plus enterprises and bodies profiled in this Yearbook, with a regulatory framework that can offer huge business opportunities for a globally focused industry.

In parallel, the Irish economy has continued to boom – with the recent improvements in the Exchequer, and the sovereign debt position of the economy showing no signs of moderating as it continues to outpace other economies. Indeed, the data indicate that ‘Ireland Inc’ is increasing its lead over the rest of the chasing pack, replicating earlier metaphors from recent history, of ‘Celtic Tigers’, or ‘Leprechaun economics’, suggesting perhaps the need of yet another new label to describe the international out-performance of the Irish economy in the 2020s.

The funds industry and aviation finance industries

The funds industry and aviation finance industries are cases in point. One is heavily regulated, and indeed, derives its very existence from the regulatory framework that it operates within. The other is largely unregulated, but yet both have thrived in Ireland in the decade since the GFC.

They have also both continued to recover in 2022, which has seen the continued recovery from another ‘black swan’ event, Covid, followed by another, the February 24th 2022 invasion of Ukraine.

Consolidation in the funds industry has been dramatic, with the rise of Third Party Management Companies one phenomenon of a business model for the asset management industry that has been pioneered in both Luxembourg and Ireland, the EU’s two fastest growing, and, income-wise, affluent financial centres in the Union.

Remarkable also has been the fact that regulatory development in one case has been to the fore in pressing change, while regulation, excluding the civil aviation sphere, has been absent in the Irish aircraft leasing sector. These themes have surfaced again in the context of the Irish relationship with the UK, post Brexit, and how, and if, the UK continues on a significantly divergent regulatory path from the European Union.

The jury will remain out on this in 2023, and probably for some time beyond that, as the UK and EU probe new frontiers under the new Sunak Government, with the evolution of the Windsor Framework, not an insignificant part of that jigsaw.

These issues already have been flagged as central to the considerations of the Irish Government by the new Minister of State, Jennifer Carroll MacNeill, who already in the first month of her tenure has had meetings with key UK FS policy figures, notably the UK Economic Secretary, and the Mayor of the City of London, Nicholas Lyons. Lyons is a son of the Irish historian FSL Lyons, and whom is to be succeeded in the post in November 2023, by another person with intimate knowledge of the Irish FS industry, Prof Michael Mainelli, a former international consultant for the Irish Government (a regular columnist in Finance Dublin and speaker at Finance Dublin events in recent years).

This is no different than it ever has been. It is proof positive of the developmental role robust and quality regulation can have, and the historical reality that finance and financial services cannot exist, let alone thrive, outside of a strong state framework. In particular, one that enables a balance between the extremes of the metaphorical ‘light touch’ regulation, popularised in the 1980s-90s, and the unmitigated promulgation of statist and regulation-heavy solutions, has proven most successful in international development case studies of financial services development.

The Irish model has been an exemplary case of this, and 2022 saw this in action, while the prospects for 2023 and beyond are for more of the same, certainly to judge by the roadmap set out by the new Minister Carroll MacNeill (see Finance Dublin, February 2022), and in her article appearing in this publication (page 10).

“The third largest funds sector in the world”

In funds, government regulatory development of fund management companies, in the form of the Central Bank of Ireland’s “CP86”, originally set out in 2014, and effectively codified in the follow up “Dear CEO letter” of 2020, set out a template model in particular for the form of third party management companies that should and could be formed, and regulated in Ireland. This framework has been evolving during the past decade, but in 2022 it gained serious traction as the industry embraced it, as reflected in a spate of consolidation, mergers and acquisitions. These are providing crucial new cogs in the investment funds servicing model of Ireland, one of the two leading EU hubs for global investment funds, Luxembourg, with its own distinctive structures and regulation being the other.

The past year has seen the accelerating use of the Irish ICAV as a funds structure, and the development of third party management companies – such as Carne, Waystone and Apex, all with strong Irish entrepreneurial DNAs which have attracted outside PE investment and are developing their models and corporate organisations, much of it through mergers and acquisitions.

This consolidation trend has been mirrored in other parts of the Irish funds ecosystem where M&A activity has also been evident, for example in admin and custody spheres, reflected by deals involving State Street, and BBH (unconsummated), and RBC ITS and Caceis, the latter scheduled to be consummated in Autumn 2023.

The upsurge in deals activity, both in M&A and debt and equity financing in capital markets in the aviation finance and funds sectors has been matched in other parts of the Irish financial services industry also. Indeed, end year data for M&A transactions in 2022 shows that the financial services sector led the way in all sectors of the Irish economy in dealmaking activity in 2022.

Speaking about the evolution of the Irish investment funds industry in particular, Sharon Donnery, the Deputy Governor of the Irish Central Bank, in a wide-ranging address to the annual dinner of the Financial Services Ireland in December 2022 said: “We have the third largest funds sector in the world. To give you a sense of the changing nature of the system, by the end of 2021, there were nearly 10,000 regulated entities, up from about 6,000 in 2016. In the same period, asset values of these entities increased from approximately €3 trillion to €5.6 trillion.

“We are seeing a very different pipeline of firms applying to become regulated - firms with novel business models, and firms applying for a number of parallel authorisations. We are seeing some firms do not understand that authorisation is just the beginning. Authorisation commences a regulatory and supervisory relationship that will continue for the duration of a firm’s existence as a regulated entity. So the nature of firms’ initial engagements with us inform our understanding of how they will approach regulatory compliance if and when they are authorised.

“Our experience has been and continues to be that firms which understand their proposed business model, the risks inherent in that and the compliance obligations in place to protect the wider system, are the firms which find the authorisation to be most straightforward. Ireland is a global financial services centre. We are confident that a credible and thorough authorisation process is part of that story and the continued growth of the sector here.”

“Ireland is a global financial services centre”

Donnery, and the Central Bank’s vision here is of Ireland as ‘a global financial services centre’ where “firms which understand their proposed business model, the risks inherent in that and the compliance obligations in place to protect the wider system, are the firms which find the authorisation to be most straightforward”. This lies at the core of the regulatory approach of the Irish authorities, from both regulator and government level, and sends a clear message regarding the attractiveness and obligations, and the inclusive, EU-centred model that is in place.

A busy regulatory agenda lies ahead, generated both at Irish national level, the roll out of the Senior Executive Accountability Framework (SEAR), being just one example in Ireland, and at EU level, a multitude of regulatory developments, some of which will prove over officious but much of which are inevitable parts of the long term infrastructure of financial services to be provided in Ireland, the EU and globally.

Another truly global industry is aircraft leasing, responsible for funding approximately half of the world’s commercial aviation fleet, itself in GDP output terms responsible for approximately 3% of the world’s business revenue.

That international industry is largely centred in Ireland, and it has had a globally dramatic, and traumatic experience over the past three years, first, due to the catastrophic effects on global civil aviation caused by Covid, and then the Russian attempt to seize Ukraine, which, was accompanied by the illegal seizure of all globally leased aircraft on Russian soil at the outbreak of the invasion of Ukraine.

Irish-based and headquartered lessors have played an enormous role in supporting the world’s airlines through the biggest crisis they have ever faced. Most of those carriers became dependent on government loans to survive the pandemic, something that compromised their balance sheets.

During the pandemic the world’s airlines increased their debt burden by about $220 billion to $650 billion, while net losses over the three-year period 2020 to 2022 erased profits made in the preceding nine years. At the same time many airlines have used the opportunity afforded by the pandemic to restructure extensively their cost structures to create competitive advantage as demand recovers, with low cost carriers in particular setting themselves up for growth.

Against this background, the largely Irish-based leasing industry has played a vital role in assisting their clients with short and long-term revisions of lease terms and with funding deliveries of new aircraft. Already responsible for close to half of all commercial aircraft flying in 2019, that proportion has increased to an estimated 53 per cent of all new aircraft and is widely expected to increase further.

The extent to which commercial aviation recovered over the past year is evident from full-year data from IATA, which shows passenger traffic recovered from 41.7 per cent of 2019 volumes in 2021 to 68.5 per cent last year. What was especially significant was the acceleration in the pace of recovery, which helped to allay fears that the initial surge in demand might be a temporary post-pandemic phenomenon.

Industry consolidation

As is the case in the Irish investment funds industry, domestic insurance and wealth management provision, consolidation was also a major theme evident in the aviation financing sector, fuelled in part by the continuing success of the AerCap takeover of GECAS. This transaction demonstrated that visionary teams within a strong and disciplined sector can create their own good fortune, not just seize opportunities. The continued bedding down of the AerCap acquisition, led by Aengus Kelly, and involving a large number of Irish professionals, both as direct employees and as outside providers of financial and legal expertise – has demonstrated the depth of expertise in the jurisdiction not just around the industry but in the legal, taxation, accounting and financial services that exist in the jurisdiction around aviation financing.

As we write elsewhere in the Yearbook: “That deal was simply not available to any other players – the underlying business imperative would have been missing and the balance sheet strain would have been too great. But despite the pandemic woes and taking a net $2.4 billion charge in Q1 in respect of assets trapped in Russia and the Ukraine, AerCap is expected to report a net income of at least $1.6 billion this year, compared to a previous forecast of $1.0 billion”.

The consolidation and development evident in 2022 has been a general phenomenon – and not limited to any particular sectors, for example funds and aviation financing. It has been evident in both the traditional Irish ‘domestic’ financial services industry and other parts of the financial services industry.

The restructuring of the domestic main banks accompanying the exit of Ulster Bank and KBC from the Irish market, with AIB and Bank of Ireland prominent in acquiring segments of the old business, including loan portfolios, as well as businesses, and with sales also of business units, and not least the state’s own engagement in the ongoing restructuring of the sector, which included in 2022 the state selling down a large proportion of its shares in AIB.

Consolidation in the domestic insurance and wealth management sectors has also been evident, Ardonagh for example. In asset management consolidation activity in REITS was again evident, as well as in portfolio companies, and, in fintech, where the innovative Irish-grown Co Cork Global Shares was acquired by JP Morgan for its global share options management expertise for a sum reported as in excess of €600m.

That there should be such dramatic and positive moves evident in the Irish financial services sectors in 2022 at a time when the global economic outlook was overshadowed by cross winds of inflation and geopolitical uncertainty is testament to the contrary experience of the Irish economy, under the radar, as it were of the global markets environment.

This was reflected, again, in 2023 by the outperformance of the Irish economy, which has continued unabated right into the early months of 2023, with the main driver, corporation tax, showing no signs whatsoever of slowing up.

Principal contributory reasons for this, and the role of the Irish Government in securing a stable agreement at OECD level, has been documented monthly in the columns of Finance Dublin in the Irish Tax Monitor.

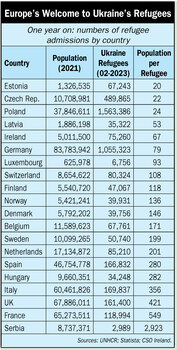

This achievement at OECD level was accomplished despite frequent global murmurings about Ireland as a tax haven with little responsibility and concern for taxpayers in other countries, in some political quarters, for example in the European Parliament. The response of Ireland as one of the leading contributors to the Ukrainian refugee crisis in 2022 (see table on page 6) in Europe was one strand of the Irish Government’s response to such criticism.

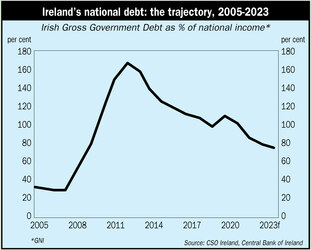

As documented in the Finance Dublin site, the Finance Dublin Debt Clock, which has tracked the evolution of the Irish national debt since 2011, there has now been a sustained drop in the debt as a percentage of national income in the past 2 years, resuming a trend that was briefly interrupted by the pandemic.

This has been on account of the truly remarkable world leading growth rates in the Irish economy in 2021, which saw the Irish debt to national income ratios turning down dramatically by some 12 percentage points of national income in the 2 years to the end of 2021.

In 2022, the trend of sharp, unprecedented cuts in indebtedness continued, and, according to data up to February 2023, the debt fell by 8 percentage points of GNP/GDP in 2022 compared with 2021.

This has brought the debt/GDP-GNP ratio in 2023 to a level approaching the levels recorded at the beginning of the Finance Dublin Debt Clock’s history in 2009, when the ratio was just 12% points lower than what it was at the end of the first quarter of 2023.

The correlation between the underlying strength of the economy, and, more importantly the reasons for that – the role of an open and diverse and stable and business positive economic environment in a single market that is the world’s largest - the EU - is strong evidence of why the broad developmental policy mix worked out over the past 60 years in Ireland continues to work for the Irish financial services industry.

In October 2022, the Department of Finance published a volume of its own history, bridging the period up to the end of the 1990s, written by UCD and now UL historian Ciaran Casey, of the previous history of the Department, up to 1959, written by Ronan Fanning. It presents what Casey describes as a ‘contrafactual’ account of the history of the period, which begins around the start of the period of the ushering in of the developmental open economy model of the Irish economy associated with one of the most famous Secretaries of the Department - T.K. Whitaker.

That postulated a developmental role of the Department contrasted with an earlier more austere approach of viewing the role of the department as largely accounting dominated - described in Fanning’s phrase as ‘the Finance view’, an Irish version of the ‘Treasury view’, originally inherited from its London counterpart.

That Government policy seems set to consolidate on this, and to bring marketing of the Irish IFS FDI package to new levels, as outlined by the new Minister of State in this year’s Finance Dublin Yearbook. That is a clear signal that at Government level the intention is to maintain the course already set.

The Minister of State for Financial Services, Jennifer Carroll MacNeill spoke with the Editor, Ken O'Brien (L) in January in an interview published in Finance Dublin on her new mandate, and contributes an article to this publication. (click to enlarge)

The funds industry and aviation finance industries

The funds industry and aviation finance industries are cases in point. One is heavily regulated, and indeed, derives its very existence from the regulatory framework that it operates within. The other is largely unregulated, but yet both have thrived in Ireland in the decade since the GFC.

They have also both continued to recover in 2022, which has seen the continued recovery from another ‘black swan’ event, Covid, followed by another, the February 24th 2022 invasion of Ukraine.

Consolidation in the funds industry has been dramatic, with the rise of Third Party Management Companies one phenomenon of a business model for the asset management industry that has been pioneered in both Luxembourg and Ireland, the EU’s two fastest growing, and, income-wise, affluent financial centres in the Union.

Remarkable also has been the fact that regulatory development in one case has been to the fore in pressing change, while regulation, excluding the civil aviation sphere, has been absent in the Irish aircraft leasing sector. These themes have surfaced again in the context of the Irish relationship with the UK, post Brexit, and how, and if, the UK continues on a significantly divergent regulatory path from the European Union.

The jury will remain out on this in 2023, and probably for some time beyond that, as the UK and EU probe new frontiers under the new Sunak Government, with the evolution of the Windsor Framework, not an insignificant part of that jigsaw.

These issues already have been flagged as central to the considerations of the Irish Government by the new Minister of State, Jennifer Carroll MacNeill, who already in the first month of her tenure has had meetings with key UK FS policy figures, notably the UK Economic Secretary, and the Mayor of the City of London, Nicholas Lyons. Lyons is a son of the Irish historian FSL Lyons, and whom is to be succeeded in the post in November 2023, by another person with intimate knowledge of the Irish FS industry, Prof Michael Mainelli, a former international consultant for the Irish Government (a regular columnist in Finance Dublin and speaker at Finance Dublin events in recent years).

This is no different than it ever has been. It is proof positive of the developmental role robust and quality regulation can have, and the historical reality that finance and financial services cannot exist, let alone thrive, outside of a strong state framework. In particular, one that enables a balance between the extremes of the metaphorical ‘light touch’ regulation, popularised in the 1980s-90s, and the unmitigated promulgation of statist and regulation-heavy solutions, has proven most successful in international development case studies of financial services development.

Sharon Donnery, Deputy Governor, financial regulation, Central Bank of Ireland: "Ireland is a global financial services centre".

The Irish model has been an exemplary case of this, and 2022 saw this in action, while the prospects for 2023 and beyond are for more of the same, certainly to judge by the roadmap set out by the new Minister Carroll MacNeill (see Finance Dublin, February 2022), and in her article appearing in this publication (page 10).

“The third largest funds sector in the world”

In funds, government regulatory development of fund management companies, in the form of the Central Bank of Ireland’s “CP86”, originally set out in 2014, and effectively codified in the follow up “Dear CEO letter” of 2020, set out a template model in particular for the form of third party management companies that should and could be formed, and regulated in Ireland. This framework has been evolving during the past decade, but in 2022 it gained serious traction as the industry embraced it, as reflected in a spate of consolidation, mergers and acquisitions. These are providing crucial new cogs in the investment funds servicing model of Ireland, one of the two leading EU hubs for global investment funds, Luxembourg, with its own distinctive structures and regulation being the other.

The past year has seen the accelerating use of the Irish ICAV as a funds structure, and the development of third party management companies – such as Carne, Waystone and Apex, all with strong Irish entrepreneurial DNAs which have attracted outside PE investment and are developing their models and corporate organisations, much of it through mergers and acquisitions.

This consolidation trend has been mirrored in other parts of the Irish funds ecosystem where M&A activity has also been evident, for example in admin and custody spheres, reflected by deals involving State Street, and BBH (unconsummated), and RBC ITS and Caceis, the latter scheduled to be consummated in Autumn 2023.

The upsurge in deals activity, both in M&A and debt and equity financing in capital markets in the aviation finance and funds sectors has been matched in other parts of the Irish financial services industry also. Indeed, end year data for M&A transactions in 2022 shows that the financial services sector led the way in all sectors of the Irish economy in dealmaking activity in 2022.

Speaking about the evolution of the Irish investment funds industry in particular, Sharon Donnery, the Deputy Governor of the Irish Central Bank, in a wide-ranging address to the annual dinner of the Financial Services Ireland in December 2022 said: “We have the third largest funds sector in the world. To give you a sense of the changing nature of the system, by the end of 2021, there were nearly 10,000 regulated entities, up from about 6,000 in 2016. In the same period, asset values of these entities increased from approximately €3 trillion to €5.6 trillion.

“We are seeing a very different pipeline of firms applying to become regulated - firms with novel business models, and firms applying for a number of parallel authorisations. We are seeing some firms do not understand that authorisation is just the beginning. Authorisation commences a regulatory and supervisory relationship that will continue for the duration of a firm’s existence as a regulated entity. So the nature of firms’ initial engagements with us inform our understanding of how they will approach regulatory compliance if and when they are authorised.

“Our experience has been and continues to be that firms which understand their proposed business model, the risks inherent in that and the compliance obligations in place to protect the wider system, are the firms which find the authorisation to be most straightforward. Ireland is a global financial services centre. We are confident that a credible and thorough authorisation process is part of that story and the continued growth of the sector here.”

“Ireland is a global financial services centre”

Donnery, and the Central Bank’s vision here is of Ireland as ‘a global financial services centre’ where “firms which understand their proposed business model, the risks inherent in that and the compliance obligations in place to protect the wider system, are the firms which find the authorisation to be most straightforward”. This lies at the core of the regulatory approach of the Irish authorities, from both regulator and government level, and sends a clear message regarding the attractiveness and obligations, and the inclusive, EU-centred model that is in place.

Waystone, Irish domiciled international Manco is one of the cluster of fast growing enterprises that are fuelling development in the global asset management industry.

A busy regulatory agenda lies ahead, generated both at Irish national level, the roll out of the Senior Executive Accountability Framework (SEAR), being just one example in Ireland, and at EU level, a multitude of regulatory developments, some of which will prove over officious but much of which are inevitable parts of the long term infrastructure of financial services to be provided in Ireland, the EU and globally.

Another truly global industry is aircraft leasing, responsible for funding approximately half of the world’s commercial aviation fleet, itself in GDP output terms responsible for approximately 3% of the world’s business revenue.

That international industry is largely centred in Ireland, and it has had a globally dramatic, and traumatic experience over the past three years, first, due to the catastrophic effects on global civil aviation caused by Covid, and then the Russian attempt to seize Ukraine, which, was accompanied by the illegal seizure of all globally leased aircraft on Russian soil at the outbreak of the invasion of Ukraine.

Irish-based and headquartered lessors have played an enormous role in supporting the world’s airlines through the biggest crisis they have ever faced. Most of those carriers became dependent on government loans to survive the pandemic, something that compromised their balance sheets.

During the pandemic the world’s airlines increased their debt burden by about $220 billion to $650 billion, while net losses over the three-year period 2020 to 2022 erased profits made in the preceding nine years. At the same time many airlines have used the opportunity afforded by the pandemic to restructure extensively their cost structures to create competitive advantage as demand recovers, with low cost carriers in particular setting themselves up for growth.

Against this background, the largely Irish-based leasing industry has played a vital role in assisting their clients with short and long-term revisions of lease terms and with funding deliveries of new aircraft. Already responsible for close to half of all commercial aircraft flying in 2019, that proportion has increased to an estimated 53 per cent of all new aircraft and is widely expected to increase further.

Carne, a long standing pioneer of the third party fund management company model grew by acquisition in 2022. (click to enlarge)

The extent to which commercial aviation recovered over the past year is evident from full-year data from IATA, which shows passenger traffic recovered from 41.7 per cent of 2019 volumes in 2021 to 68.5 per cent last year. What was especially significant was the acceleration in the pace of recovery, which helped to allay fears that the initial surge in demand might be a temporary post-pandemic phenomenon.

Industry consolidation

As is the case in the Irish investment funds industry, domestic insurance and wealth management provision, consolidation was also a major theme evident in the aviation financing sector, fuelled in part by the continuing success of the AerCap takeover of GECAS. This transaction demonstrated that visionary teams within a strong and disciplined sector can create their own good fortune, not just seize opportunities. The continued bedding down of the AerCap acquisition, led by Aengus Kelly, and involving a large number of Irish professionals, both as direct employees and as outside providers of financial and legal expertise – has demonstrated the depth of expertise in the jurisdiction not just around the industry but in the legal, taxation, accounting and financial services that exist in the jurisdiction around aviation financing.

As we write elsewhere in the Yearbook: “That deal was simply not available to any other players – the underlying business imperative would have been missing and the balance sheet strain would have been too great. But despite the pandemic woes and taking a net $2.4 billion charge in Q1 in respect of assets trapped in Russia and the Ukraine, AerCap is expected to report a net income of at least $1.6 billion this year, compared to a previous forecast of $1.0 billion”.

The consolidation and development evident in 2022 has been a general phenomenon – and not limited to any particular sectors, for example funds and aviation financing. It has been evident in both the traditional Irish ‘domestic’ financial services industry and other parts of the financial services industry.

The restructuring of the domestic main banks accompanying the exit of Ulster Bank and KBC from the Irish market, with AIB and Bank of Ireland prominent in acquiring segments of the old business, including loan portfolios, as well as businesses, and with sales also of business units, and not least the state’s own engagement in the ongoing restructuring of the sector, which included in 2022 the state selling down a large proportion of its shares in AIB.

Consolidation in the domestic insurance and wealth management sectors has also been evident, Ardonagh for example. In asset management consolidation activity in REITS was again evident, as well as in portfolio companies, and, in fintech, where the innovative Irish-grown Co Cork Global Shares was acquired by JP Morgan for its global share options management expertise for a sum reported as in excess of €600m.

That there should be such dramatic and positive moves evident in the Irish financial services sectors in 2022 at a time when the global economic outlook was overshadowed by cross winds of inflation and geopolitical uncertainty is testament to the contrary experience of the Irish economy, under the radar, as it were of the global markets environment.

This was reflected, again, in 2023 by the outperformance of the Irish economy, which has continued unabated right into the early months of 2023, with the main driver, corporation tax, showing no signs whatsoever of slowing up.

Principal contributory reasons for this, and the role of the Irish Government in securing a stable agreement at OECD level, has been documented monthly in the columns of Finance Dublin in the Irish Tax Monitor.

This achievement at OECD level was accomplished despite frequent global murmurings about Ireland as a tax haven with little responsibility and concern for taxpayers in other countries, in some political quarters, for example in the European Parliament. The response of Ireland as one of the leading contributors to the Ukrainian refugee crisis in 2022 (see table on page 6) in Europe was one strand of the Irish Government’s response to such criticism.

As documented in the Finance Dublin site, the Finance Dublin Debt Clock, which has tracked the evolution of the Irish national debt since 2011, there has now been a sustained drop in the debt as a percentage of national income in the past 2 years, resuming a trend that was briefly interrupted by the pandemic.

This has been on account of the truly remarkable world leading growth rates in the Irish economy in 2021, which saw the Irish debt to national income ratios turning down dramatically by some 12 percentage points of national income in the 2 years to the end of 2021.

In 2022, the trend of sharp, unprecedented cuts in indebtedness continued, and, according to data up to February 2023, the debt fell by 8 percentage points of GNP/GDP in 2022 compared with 2021.

This has brought the debt/GDP-GNP ratio in 2023 to a level approaching the levels recorded at the beginning of the Finance Dublin Debt Clock’s history in 2009, when the ratio was just 12% points lower than what it was at the end of the first quarter of 2023.

The correlation between the underlying strength of the economy, and, more importantly the reasons for that – the role of an open and diverse and stable and business positive economic environment in a single market that is the world’s largest - the EU - is strong evidence of why the broad developmental policy mix worked out over the past 60 years in Ireland continues to work for the Irish financial services industry.

In October 2022, the Department of Finance published a volume of its own history, bridging the period up to the end of the 1990s, written by UCD and now UL historian Ciaran Casey, of the previous history of the Department, up to 1959, written by Ronan Fanning. It presents what Casey describes as a ‘contrafactual’ account of the history of the period, which begins around the start of the period of the ushering in of the developmental open economy model of the Irish economy associated with one of the most famous Secretaries of the Department - T.K. Whitaker.

That postulated a developmental role of the Department contrasted with an earlier more austere approach of viewing the role of the department as largely accounting dominated - described in Fanning’s phrase as ‘the Finance view’, an Irish version of the ‘Treasury view’, originally inherited from its London counterpart.

That Government policy seems set to consolidate on this, and to bring marketing of the Irish IFS FDI package to new levels, as outlined by the new Minister of State in this year’s Finance Dublin Yearbook. That is a clear signal that at Government level the intention is to maintain the course already set.