This month’s roundtable discusses the potential impact on the FS industry of the amendments introduced in the Finance Bill to the anti-avoidance provisions in S.110 TCA 1997. The changes provide for stronger provisions and put the tax avoidance main purpose test on an objective footing.

Implementation of the EU’s mandatory disclosure regime for cross-border transactions, ‘DAC6’, is another area not addressed as part of the Budget but which will require significant further clarification. DAC6 must be introduced into Irish law by the end of this year but will apply retrospectively to the date at which the Directive came into force, 25 June 2018.

Practical issues, such as reporting mechanisms and administrative concerns, will be a key focus to ensure duplicate reporting is minimised wherever possible. In this roundtable we also look at the value of investing in technologies in the Fintech, analytics, cognitive and robotic process automation space for regulatory and financial reporting purposes and how this can be addressed initially using time-boxed ‘experiments’ to identify appropriate technologies.

With Brexit an unending source of uncertainty, the roundtable also reflects on the way in which it will affect supply chains/logistics, warehousing, cash flow, invoicing, IT processes and VAT reporting. Its possible effects on direct taxation are likely to be less, however, as Ireland will continue to hold its double tax treaty with the UK.

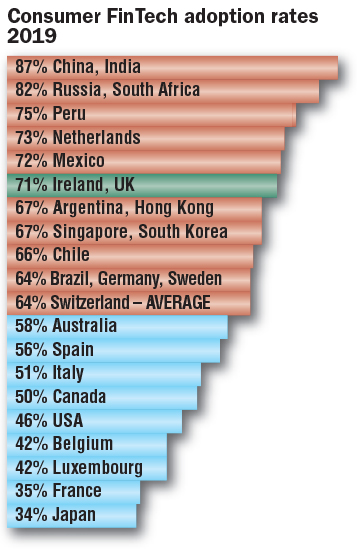

Ireland outperforms on FinTech adoption

Ireland outperforms on FinTech adoption