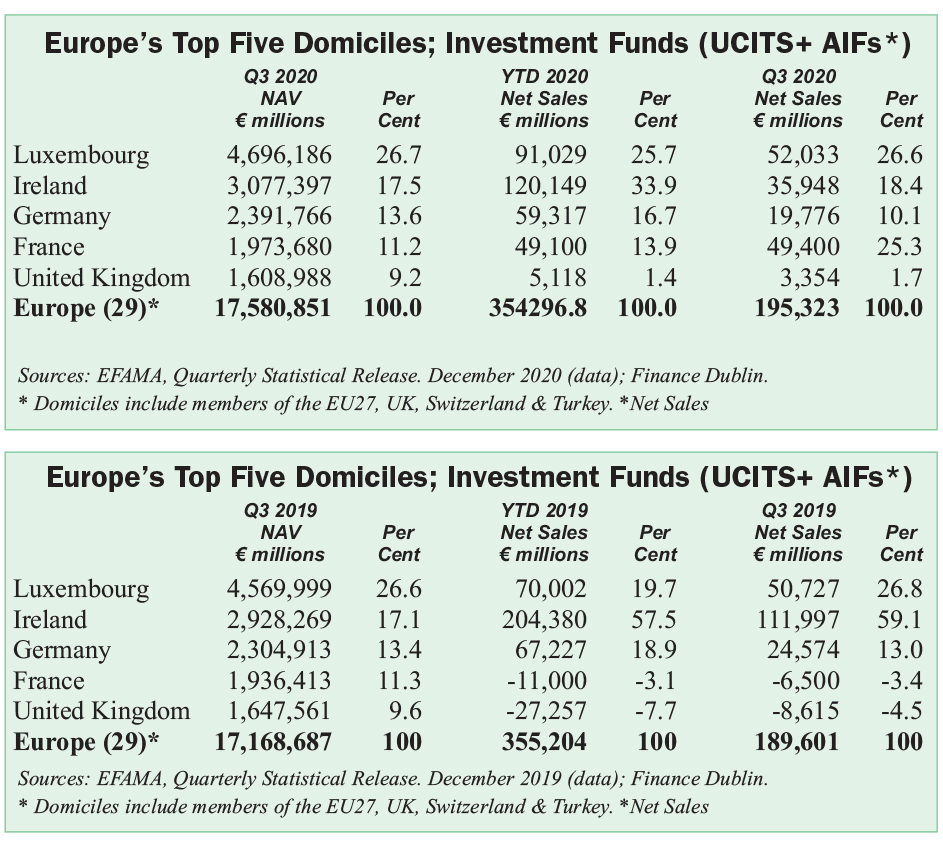

The global economy, asset managers and the investment funds industry have experienced a year of special challenges that sees the pandemic pass as the first concern, to questions as to how the aftermath can be negotiated. Intensified competition in fees, and tech and regulatory challenges, not least in Europe and Ireland add to a business environment that sees a flurry of new acquisition activity as the consolidation of Ireland as a funds domicile takes place on the eve of Brexit, a process confirmed in the latest statistics for funds NAVs shown in the tables on this page.

As markets recover to reach record levels after a year that whipsawed in equity markets, and new asset classes promise to come into vogue, such as commodities and cryptocurrencies, funds professionals are looking to 2021 with renewed interest as to how they can unlock the investment advantages of the current era to the advantage of their clients, fund investors.

This concern is evident in the contributions of leading players in the industry, illustrated in the articles appearing in this Report, and in the Questions and Answers in our first Roundtable edition of the Finance Dublin Funds Monitor, which appears in page 26.

This concern is expressed for example by reference to challenges in enabling opportunities to obtain access for investors to previously hard to access asset classes like real estate, by Ross McCann, head of fund services at Alter Domus, Ireland and by RBC I&TS’s Ronan Doyle who cites a panel he chaired at a Fund Forum International digital event in October considering how illiquid assets could be better 'retailized'.

This commercial focus must remain first and foremost in the minds of every funds professional, not least the 10,000 plus strong Irish investment funds industry which continues to grow, and which received a Christmas present at the end of the year from the new Coalition Irish Government (formed in May) in the form of passage of the Investment Limited Partnerships Bill into legislation, providing the jurisdiction with a key funds wrapper that it lacked, compared with Luxembourg, (Europe’s largest funds domicile - see table on this page) for example.

The Irish Funds Representative body Irish Funds estimated that the ILP alone will lead to €20bn p.a. in global private capital being attracted and 3,000 new jobs being created in the Irish funds sector over the next five years, adding to the existing 16,000 employees nationally.

Irish funds CEO Pat Lardner commented: ‘Ireland has today reasserted its position as a leading, full-service location for the global funds industry and I congratulate Government and the Minister for Financial Services Sean Fleming TD, on this milestone.

‘This is game-changing in terms of Ireland’s global competitiveness and will enable and drive new business and opportunities, as well as retain business which has previously been lost overseas. It will help develop Ireland as a centre for green financing and align us with EU policy goals in sustainable finance’, he said.

This Irish legislation (details of which are explained in this Report by Dillon Eustace Partner Derbhil O’Riordan on page 23) is just one element in a scheduled series of regulatory and legislative developments that will engage the minds of the industry in 2021.

Also in Ireland, there can be expected to be developments under the SEAR heading, as qualifications of senior executives in the industry come under scrutiny. Also, on the cybersecurity front, there will be major work at play across the funds industry spectrum in Ireland as the Central Bank leads the charge there, notably in the form of its advice to funds companies to appoint Chief Information Officers to overlook security issues.

The governance agenda led by the Central Bank extends even to tax matters, which is put in context of the overall governance agenda from the CBI by Deloitte’s Seamus Kennedy on page 14.

Of course, at EU level, there is an agenda too, notably the incomng ESG-related process to be ushered in by the Sustainable Finance Disclosure Regulation (SFDR), details of which are set out in an article by Simmons & Simmons lawyers Niamh Ryan and Hazel Doyle on page 12.

ESG is a game changer across the financial services industry, and not least in asset management and investment funds.

To quote Donncha Morrissey, Head of Ireland’s Branch, Sparkasse Bank Malta plc: in the first edition of the Finance Dublin Funds Monitor, on page 26: ‘2021 really bring us to a new phase in the ESG landscape with the Sustainable Finance Disclosure Regulation (‘SFDR’), which was agreed last year being phased in from March 10 2021. This new phase brings with it mandatory environmental social governance (ESG) disclosure obligations for asset managers directly and its products offered’.

Distribution and marketing, and regulatory issues are intertwined, as 2020, the year of Covid-19, has underlined to the entire planet.

The volatility experienced in the initial months of the pandemic, particularly in March-April put systemic risk issues to the forefront, for both Central Banks and regulators and institutions, such as custodian banks like Northern Trust, State Street and RBC, but it has been reassuring that despite instances of liquidity squeezes, referenced by Paul Stillabower Head of Product and Profitability, Core Services at RBC Investor & Treasury Services (RBC I&TS), the system systemically has been robust.

An ongoing focus on potential liquidity mismatches may help avert the risk of liquidity squeezes for investment funds, he concluded.

Regulators are carefully examining liquidity risk management for certain open-ended funds (e.g., real estate). Despite being delayed because of COVID-19, the UK FCA and Bank of England are conducting a review into the daily dealing practices of such funds. As the COVID-19 experience has shown, liquidity mismatches can result in trading suspensions. And while it is an infrequent event, nonetheless, every suspension represents a failure to deliver to investors the key distinguishing feature of an open-ended fund–the ability to have their investment redeemed on a date of their choosing.”

His colleague Don D’Eramo, Global Head of Securities Finance at RBC Investor & Treasury Services report on the securities lending industry 's robust response to the crisis, as volatility soared in the early months was reassuring. There were no fail trades or losses, despite the appearance of spikes in underlying sectors such as aviation and tourism, he said.

In individual sectors, the historic unlocking of opportunity for investor, in the development of products like ETFs, and the overall passive investing model continue to show their long term resilience, as Lisa Kealy and Kieran Daly points out in their article on page 18, focussing on the year for ETFs in 2020 to date.

Kealy, who took up the role of chair of Irish Funds in May 2020, (in the first virtual online appointment process) putting ETFs in wider context says: “The performance of ETFs during market stress is not the only factor that argues for continued AUM growth into the 2020s. The industry’s historic growth drivers, including the shift to passive and the structural decline of fees, remain in force. Other trends reshaping the investment industry - like the tendency of smart beta and factor investing to replace core active, the increasing demand for high standards of transparency, and the need for individuals to take more responsibility for long-term savings - should also favour ETFs’.

Security questions and transactional costs in asset management are central as well in asset servicing, and outsourcing. and technology’s advance in 2020 has been relentless. are also important.

Meliosa O’Caoimh, Northern Trust’s Country Head, Ireland identifies particular opportunities in the asset servicing sphere in the areas of transfer agency and fund accounting. “The opportunity is not just to move processes online, but to leverage technology to significantly improve business practices and reimagine these functions for the digital age”, she says, (page 27).

‘Improving the quality, speed and governance of investment data will be key to this digital transformation. By offering more high-quality data quicker, asset servicers will be able to drive enhanced operational efficiencies and help asset managers create new digital experiences, both for themselves and their investors. This means, for example, enabling asset managers to interact with their investors flexibly and coherently, and to be able to see all their investments in a single place”, she says.

Brexit has resulted in a huge stimulus to the fund management industry in Ireland as it is increasingly being seen as a platform for former UK distributors to market and deliver their products in the European Union.

Coinciding with this has been the response of the Central Bank of Ireland to define, clarify, and develop its regulatory framework for the jurisdiction, in various initiatives during 2020, summarised in numerous initiatives referenced in this report, including its thematic (CP86) review.

Bridge Consulting director David Dillon, for example, comments on this in his article on page 16.

He says that much of this has been prompted by the findings at the CBI that when applied correctly by firms, the rules and guidance provide a framework of robust governance and oversight arrangements. ‘The CBI has taken the view that the framework has provided a strong basis for firms to identify and retain the level and nature of resources needed and to put in place the required governance, management, systems and controls but that a number of previously authorised FMCs have not fully implemented the framework.

‘The CBI identified a number of areas of weakness including resourcing, delegate oversight and performance of some designated individuals. This has prompted the CBI to introduce a number of requirements and it anticipates further requirements’, he says.

As asset managers navigate the more competitive and volatile market of 2020, there has been an enhanced focus on operational models, with consideration of the further gains to be achieved from outsourcing, and, along with that the opportunities to obtain access for investors to previously hard to access asset classes like real estate. Ross McCann (page 24) head of fund services at Alter Domus, Ireland spoke to Finance Dublin about the particular opportunities around that asset class:

“Even before the pandemic, there was a trend towards more outsourcing for well-rehearsed reasons. Real estate managers’ operations are often highly complex, stretching across international borders. They involve multiple layers of special purpose vehicles as well as different parties; and reporting must be consolidated across multiple jurisdictions, often with their own currency, accounting standards and regulatory compliance requirements.

“Ireland is no different,” McCann added, “with ICAVs, SPVs and, soon, Investment Limited Partnerships forming part of both global investment fund structures and local stand-alone structures.” On the ground, such funds are helping transform towns and cities through the delivery of signature commercial buildings, apartments, housing and infrastructure, as well as vital investment in warehousing and logistics”.