As failure in each case would require supervisory intervention under Solvency II, EIOPA recommends that national supervisory authorities and the relevant companies start the process now. Ireland is not immune either, being one of a number of countries where ‘more than 10% of entities’ failed to cover their SCR under the baseline scenario.

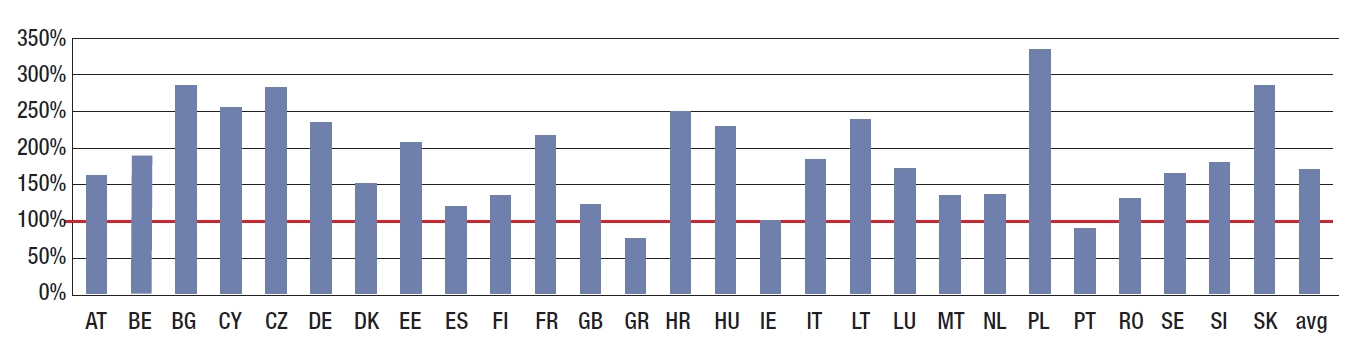

Pre stress SCR Ratios (weighted by SCR). Low Yield Sample. Source: EIOPA Insurance stress test report 2014. (click to enlarge)

The stress test consisted of two modules. The first was a “Core Module” focussed on groups and the effect of a range of asset or single factor insurance stresses. This found that while 86% of companies under the baseline scenario had an SCR ratio of over 100%, 14% did not and 8% would not have been able to cover their MCR. If the Long Term Guarantee mitigating measures allowed under SII were not taken advantage of the number failing to cover the SCR would rise to 19%. Under the first of the stress scenarios, which is assumed to be instigated by a fall of 41% in equity markets, the percentage of companies with an SCR ratio of less than 100% increased to 44%. Under the second stress scenario, initiated by a widening of corporate bond spreads, the percentage with an SCR ratio below 100% was 27%.

The second module, called the Low Yield module focussed on individual entities under two scenarios - a persistent Japanese like low yield environment and an “inverse” scenario with an atypical change in the shape of the yield curve. Overall the baseline results were similar to the Core Module with 84% of entities having an SCR ratio in excess of 100% and 16% falling below. Under the two stress scenarios the percentage of companies with an SCR ratio below 100% increased to 24% and 20% respectively.

The stress test results come with a lot of caveats - for example the standard formula is used by all companies. However the sampled companies cover 55% of gross written premiums and 60% of technical reserves so the results can be considered representative. Individual company results are not being released but the data from the second module is analysed by country of incorporation.

This is perhaps the most interesting and, from an Irish perspective, the most worrying part of the results. While the average SCR under the baseline scenario across the EU was about 160%, in Ireland (IE in the above chart) it was only about 100% and “more than 10%” of entities fell below the 100% SCR ratio. Only Greece (GR) and Portugal (PL) had lower ratios, although the UK (GB) was only about 125%. Germany (DE) in contrast had an aggregate ratio of well over 200% and Italy’s (IT) was about 180%. On the positive side the Irish liabilities seem to be well matched and the stress scenarios did not worsen the situation.

The report also points out that the unweighted SCR ratio for some countries, including Ireland, is considerably higher than the weighted average quoted above (at least 25 percentage points), suggesting that larger contributors in terms of SCR have a coverage ratio well below the others within the national sample or that there were a number of outliers distorting the overall result.

The Irish companies that participated in the second module were Axa Insurance, Canada Life International Re, Hannover Re, FBD, Irish Life, Liberty Insurance, New Ireland, RSA Insurance, XL Group, XL Re Europe, Zurich Insurance PLC and Zurich Life Assurance.