John Lyons

This article covers the life assurance results and another article in Finance Dublin analyses the non-life results. Overall the life market (new single premiums and annual premiums combined) was up 13.6% in 2013 from €22.1bn to €25.1bn.

The domestic business, including branches of foreign companies, was up 17% from €5.3bn to €6.2bn - the best result since 2010 but still a long way short of the €12.9bn attained in 2007. The international business was up 12.5% from €16.8bn to €18.9bn, the second highest result ever - eclipsed only by 2007 when €19.7bn was achieved.

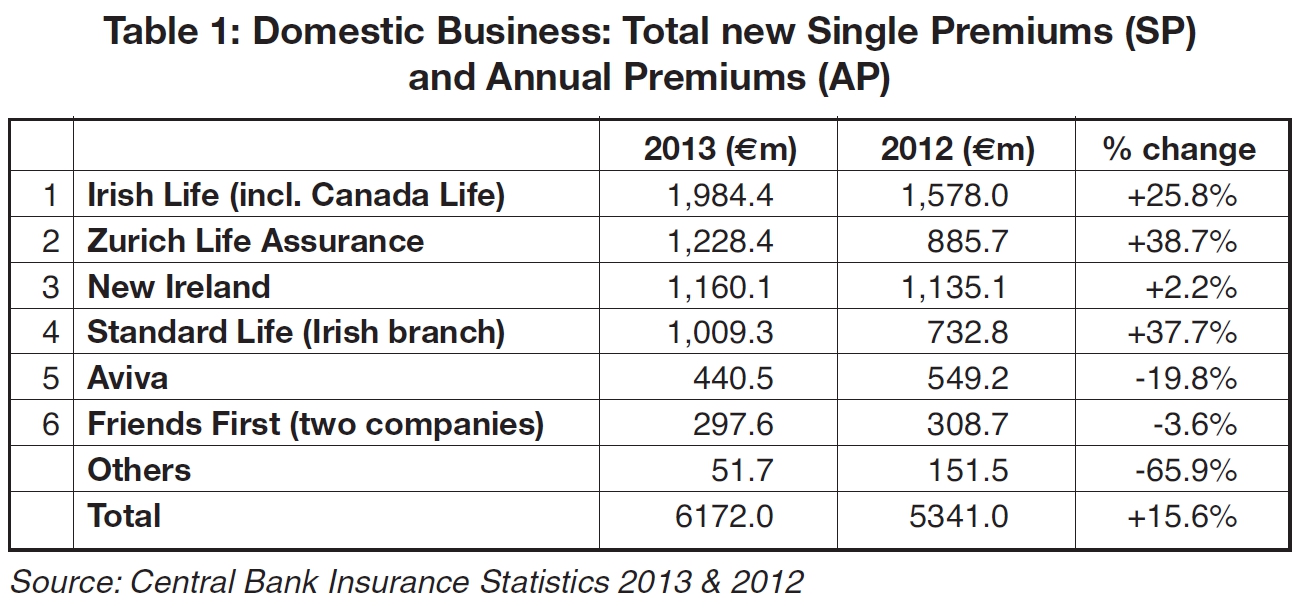

Domestic business

The Irish risk business saw further concentration in 2013 with the acquisition of Irish Life by the Great West Life Group which already owned Canada Life Ireland. Combining the two Great West companies, the top six players in 2013 accounted for 99.2% of new business.

The growth in 2013 was concentrated in Single Premium business (up 16.9% from €5.0bn to €5.8bn) with new Annual Premium business actually slightly down (2.3% from €362m to €354m). The single premium results from Zurich and Standard life are particularly impressive, with the combined Irish Life/Canada Life results also showing strong growth – it will be interesting to see whether these businesses prove additive when the 2014 results become available.

Total premiums, including recurring premiums, were €10.5bn for the year, comprised of €8bn single premiums and €2.5bn annual premiums. This was an increase of 13.2% on 2012 but total claims rose even more - by 16% from €10.6bn to €12.3bn. Investment income and gains however ensured that total funds (Irish Head Office companies only) still managed to increase over the year - from €65.8bn to €68.7bn.

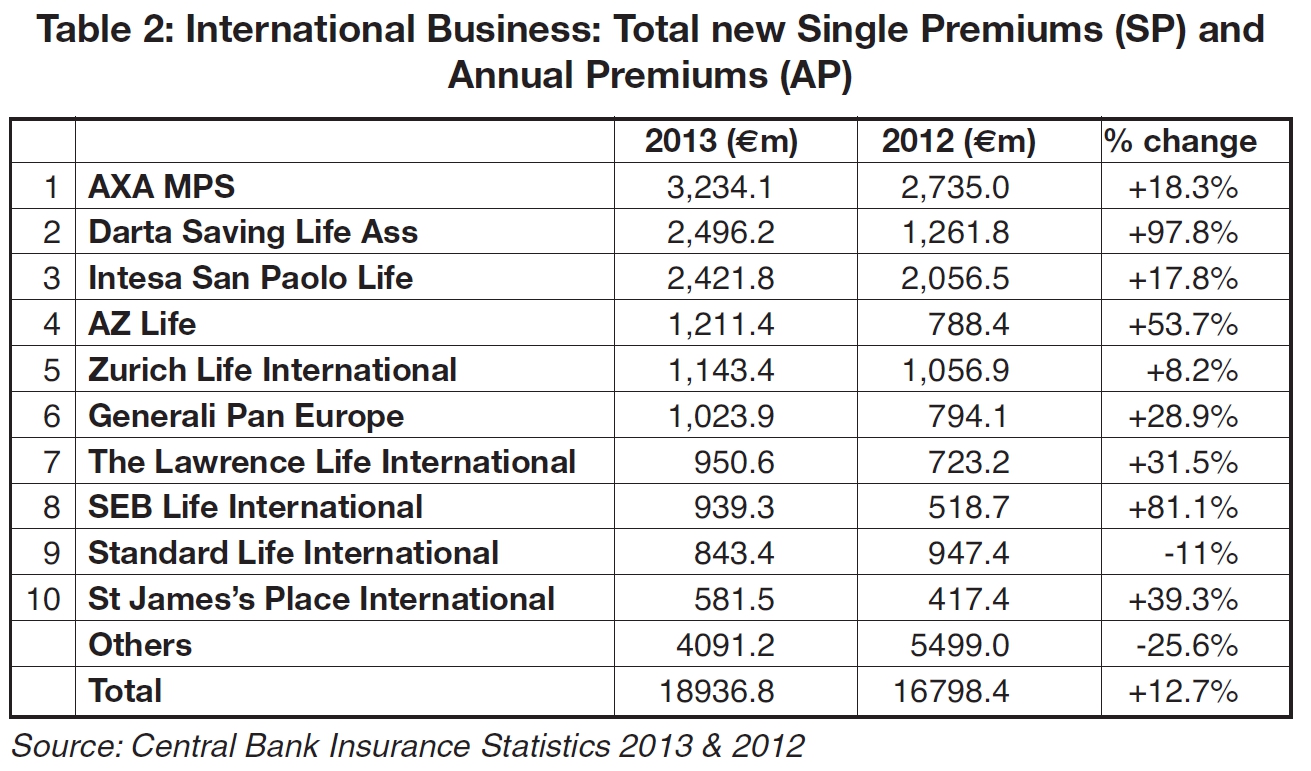

International business

The International life business in 2013 continued to be dominated by single premium business which accounted for 98.8% of total new premiums. The top 10 players can be seen in Table 2.

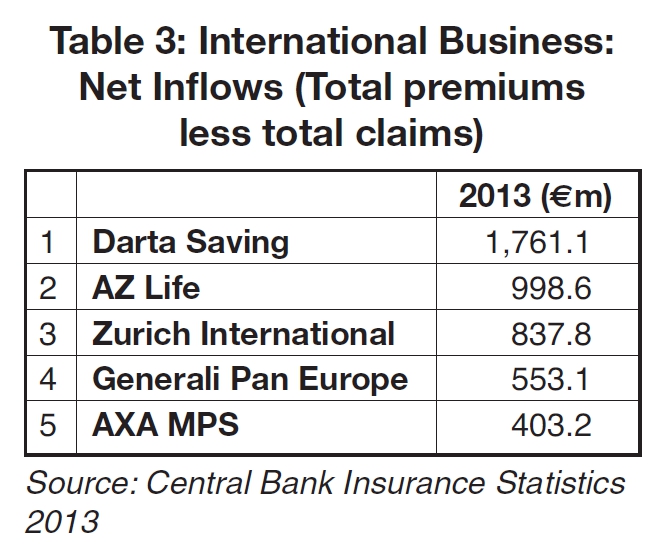

Darta Saving, SEB Life International and AZ Life showed the strongest growth in the year and only Standard Life International among the top ten companies showed a decline. AXA MPS was again the biggest company in terms of overall new business. However AXA MPS and some of the other companies also had high claims levels and when one looks at net inflows the top 5 table is actually quite different:

Overall net inflows were positive for the international life sector with total premium income (including recurring premiums) of €20.5bn comfortably exceeding total claims of €14.5bn. Including investment income and gains, total funds of the sector increased from €89.3bn to €98.7bn.

Insurance Ireland FactFile

The Insurance Ireland FactFile 2013 covers international life business for the first time, reflecting the increased focus by the organisation on the sector since the arrival of its new CEO Kevin Thompson. Although the analysis only covers 16 members of its wider international membership this includes nearly all the big players and, with €12.5bn in new premiums, some two thirds of the total sector.

The Insurance Ireland numbers are broadly consistent with the Central Bank numbers except in relation to MetLife Europe where they show MetLife with total new premiums of €1.487bn (€1.216bn SP and €271m AP) compared with the Central Bank’s €449m.

This could have arisen if MetLife has included in its Insurance Ireland numbers business that it acquired with its ALICO acquisition that has yet to be formally integrated into the Irish company. If correct it would put Met Life in fourth place for new business in 2013, and more than double the total AP written by the sector.

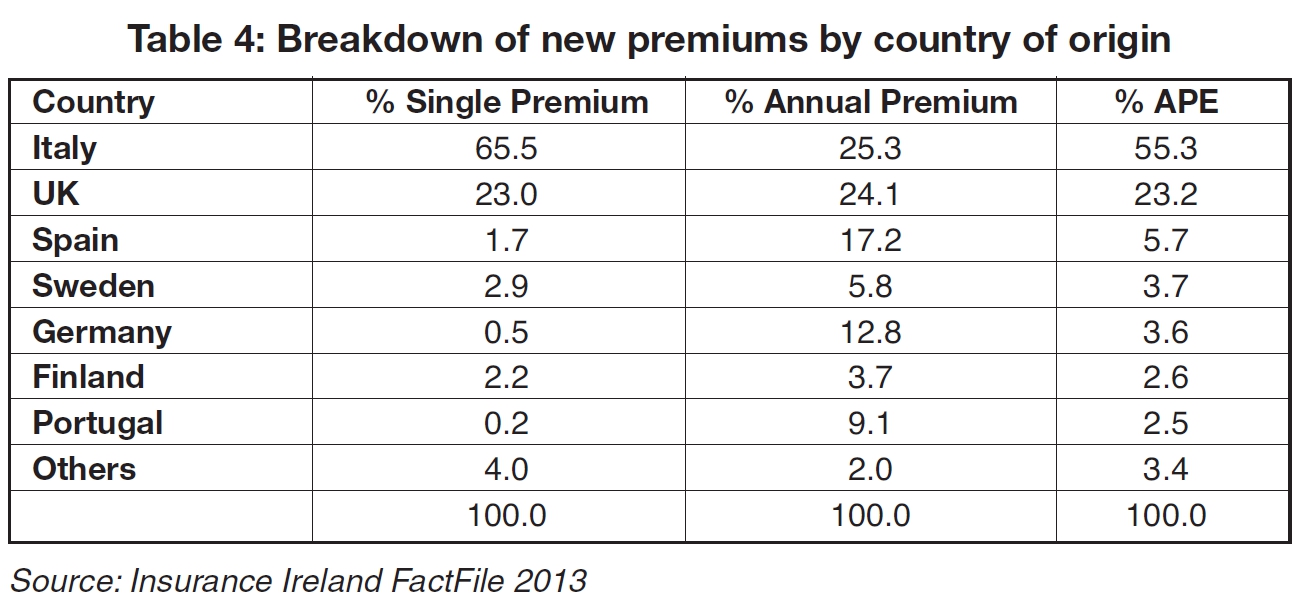

One particularly interesting analysis provided in the Insurance Ireland FactFile and not available in the Central Bank statistics is the breakdown by business by country of origin.

Not surprisingly Italy is by far the biggest market representing 65.5% of SP and 25.3 % of AP, or 55.3% using the industry measure of APE (Annual Premium Equivalent equal to AP plus 10% SP). The UK is a strong second with 23% of SP and 24.1% of AP (23.2% of APE). The figures for the other markets are intriguing as can be seen in Table 4 constructed from the II numbers and ranked by APE:

There is no further breakdown of these numbers in the II data but anecdotally it is believed that the Swedish and Finnish sales are dominated by SEB International for which these are ‘home’ markets. The German business is predominantly a regular premium one and most of the sales here come from Canada Life Europe. Spanish business seems to be spread over a number of companies - Generali Pan Europe, SEB, St James Place, Prudential and Met Life are all involved, as is Mediolanum among non-survey companies. The Portuguese business is thought to be mainly from Met Life.